How Property Taxes Work in the United States

Property tax is the single largest source of revenue for local governments across the United States. According to the U.S. Census Bureau, local governments collected over $730 billion in property tax revenue in 2022, funding schools, roads, emergency services, and public infrastructure. Unlike income tax — which is calculated on earnings — property tax is based on the value of real estate you own.

The basic formula behind every property tax bill is: Assessed Value × Tax Rate = Property Tax. But the details behind that formula — assessment ratios, mill levies, exemptions, and abatements — make the system far more complex than it appears. Every homeowner in America pays property tax, but the amount varies enormously depending on where you live.

Understanding Effective Tax Rates vs. Nominal Rates

When comparing property taxes across states, the effective tax rate is the most useful metric. The Tax Foundation defines the effective property tax rate as total property taxes paid divided by total home value. This differs from nominal or statutory rates because it accounts for assessment ratios and exemptions that reduce the taxable base.

For example, according to Tax Foundation data, Louisiana assesses homes at only 10% of market value and offers a $75,000 homestead exemption, resulting in an effective rate of just 0.52%. Meanwhile, New Jersey assesses at full market value and has limited exemptions, resulting in an effective rate of 2.23% — the highest in the nation.

This gap means two homes with identical market values produce wildly different tax bills. A $350,000 home in New Jersey faces roughly $7,800 in annual property tax. The same $350,000 home in Hawaii — where the effective rate is just 0.27%, according to Tax Foundation rankings — would owe approximately $950 per year.

Property Tax by State: The Full Picture

According to the Tax Foundation's annual property tax analysis, states with the highest effective rates are concentrated in the Northeast and Midwest, where local governments rely heavily on property tax revenue. States with lower rates often supplement revenue through higher sales taxes, income taxes, or natural resource extraction.

Highest Property Tax States

Based on Tax Foundation data and U.S. Census Bureau American Community Survey estimates, the five states with the highest effective property tax rates are:

| State | Effective Rate | Median Tax Paid | Median Home Value |

|---|---|---|---|

| New Jersey | 2.23% | $8,928 | $401,400 |

| Illinois | 2.08% | $4,942 | $239,100 |

| Connecticut | 1.96% | $6,153 | $313,600 |

| New Hampshire | 1.86% | $6,388 | $361,700 |

| Vermont | 1.83% | $4,987 | $272,400 |

Sources: Tax Foundation, Property Tax Rankings (2024); U.S. Census Bureau, American Community Survey.

Lowest Property Tax States

According to the same Tax Foundation analysis, the five states with the lowest effective property tax rates are:

| State | Effective Rate | Median Tax Paid | Median Home Value |

|---|---|---|---|

| Hawaii | 0.27% | $1,971 | $722,500 |

| Alabama | 0.37% | $646 | $172,800 |

| Colorado | 0.49% | $2,267 | $466,200 |

| Arizona | 0.51% | $1,788 | $349,700 |

| Louisiana | 0.52% | $963 | $184,800 |

Sources: Tax Foundation, Property Tax Rankings (2024); U.S. Census Bureau, American Community Survey.

What Determines Your Property Tax Bill

Four main factors drive your property tax bill. Understanding each one helps you identify where savings might be possible.

1. Market Value Assessment

Your local assessor estimates your home's market value based on comparable sales, property characteristics, and sometimes cost-replacement approaches. According to the International Association of Assessing Officers (IAAO), most jurisdictions reassess property values on a 1-to-6-year cycle. If your assessment doesn't reflect your home's true market value, you may be overpaying.

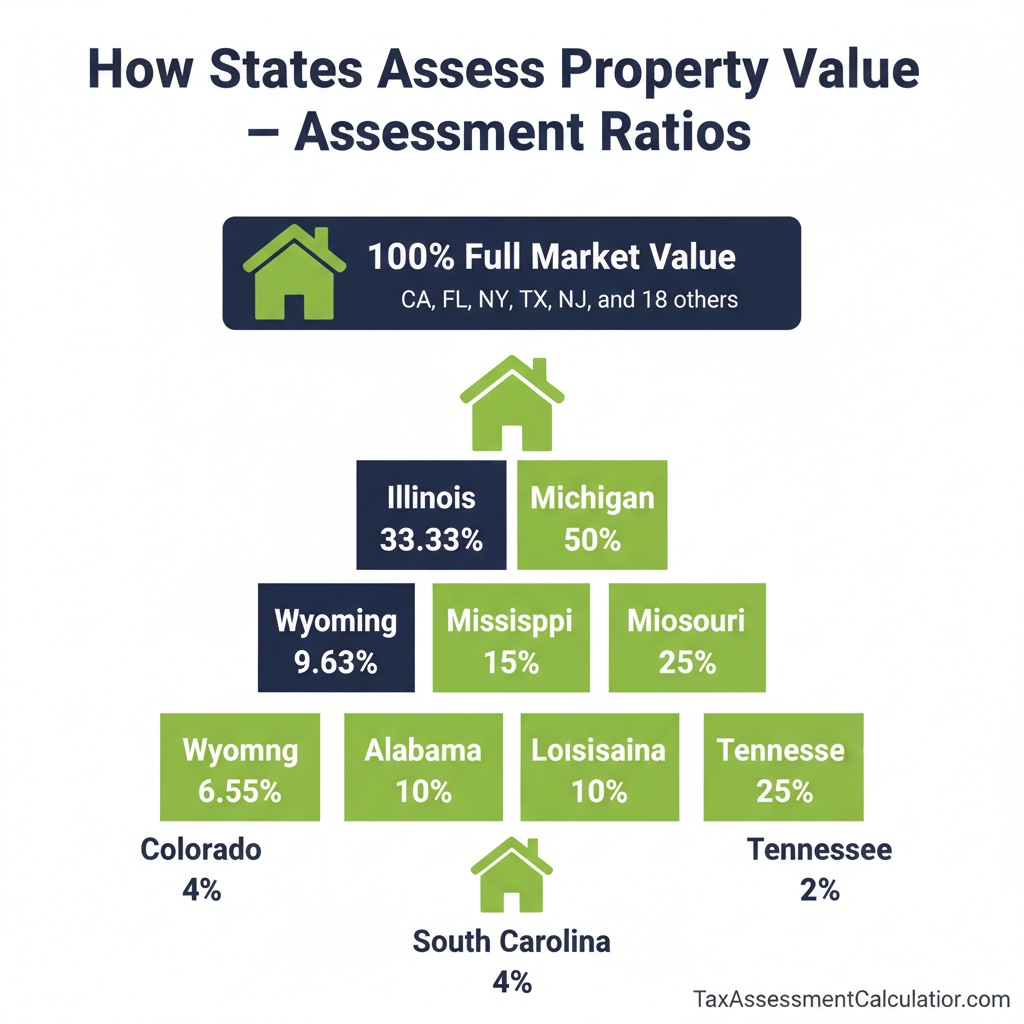

2. Assessment Ratio

Most states don't tax the full market value. Instead, they apply an assessment ratio — a percentage that converts market value into assessed value. According to the Tax Foundation, Colorado applies the lowest residential assessment ratio in the country at just 6.55%, meaning a $400,000 home has an assessed value of only $26,200. South Carolina assesses owner-occupied homes at just 4% of market value — the lowest of any state. By contrast, 23 states and the District of Columbia assess at 100% of market value, including California, Florida, New York, and Texas.

3. Exemptions and Deductions

Homestead exemptions reduce the taxable portion of your home's value. According to the Texas Comptroller of Public Accounts, Texas offers a $100,000 homestead exemption for school district taxes, plus an additional 20% of appraised value — one of the most generous in the country. The Florida Department of Revenue provides up to $50,000 in homestead exemption. According to the Louisiana Tax Commission, Louisiana exempts the first $75,000 of a home's market value from property tax. Many states also offer additional exemptions for seniors, veterans, and disabled homeowners.

4. Mill Rate (Tax Rate)

The mill rate is set by each taxing jurisdiction — school districts, counties, cities, and special districts. One mill equals $1 of tax per $1,000 of assessed value. Your total tax rate is the sum of all overlapping jurisdictions. According to the Lincoln Institute of Land Policy, a typical homeowner is subject to 4 to 8 overlapping taxing districts, including county, city, school, fire district, and library district levies.

The SALT Deduction and Property Taxes

Under the Tax Cuts and Jobs Act of 2017 (Public Law 115-97), the State and Local Tax (SALT) deduction is capped at $10,000 per household ($5,000 if married filing separately). According to the IRS, this cap includes both property taxes and state income taxes (or sales taxes) combined. This significantly impacts homeowners in high-tax states like New Jersey, New York, Connecticut, and California, where annual property taxes alone often exceed $10,000.

According to the Tax Policy Center, roughly 11% of tax filers claimed the SALT deduction after the cap was implemented, down from 30% before the cap. If your combined state income tax and property tax exceed $10,000, you're effectively paying the excess with no federal tax benefit — making reducing your property tax assessment even more valuable in high-tax states.

How to Reduce Your Property Tax

While you can't control the tax rate set by your local government, you can take steps to ensure you're not paying more than your fair share.

Verify Your Assessment

Start by reviewing your property record card at the assessor's office. According to the National Taxpayers Union Foundation, an estimated 30% to 60% of properties in the United States are over-assessed. Common errors include incorrect square footage, lot size, number of bedrooms and bathrooms, or property condition ratings. Even a small data error — such as a missing "fair" condition adjustment — can inflate your assessed value by thousands of dollars.

Apply for Every Exemption You Qualify For

Many homeowners miss exemptions they're entitled to because homestead exemptions typically require an application — they don't apply automatically. According to the AARP, millions of eligible homeowners fail to claim senior exemptions, veteran exemptions, and disability exemptions each year. Check with your county assessor to make sure you're receiving every exemption available to you.

Appeal Your Assessment

According to the National Taxpayers Union Foundation, homeowners who appeal their property tax assessments win reductions in roughly 30% to 60% of cases. The strongest evidence includes recent sale prices of comparable homes, an independent appraisal, and documentation of property defects. Most appeals are handled at the local level, and many jurisdictions offer an informal review with the assessor before requiring a formal hearing.